You Call It Friction, I Call It Human Experience

The Frictionless Trap: what we lost when Friction became enemy No 1.

Every brand steward has a version of this story. The moment the briefs shifted. Perhaps it arrived via a new funding round and bonkers expectations or perhaps just a new set of KPIs that did not include a column for things like wonder or wander. We started picturing the funnel not as a journey but as a series of ways to, essentially and sometimes literally, keep the customer “in line” and moving towards checkout.

Marketers who’d spent careers understanding humans and their relationships to brands weren’t absent from these conversations. We were out-hyped, out-shouted. And, this is the part that doesn’t get said out loud: marketing shifted from a job that attracted people with empathy to folks who think everything can be explained in 0s and 1s. Performance marketing came with a dashboard and created a veneer of health and speed. Everyone had the same enemy: Friction. Arguing for “brand” to a leadership that leaned into extraction wasn’t a battle that came with much armor.

Of course, our dashboards were measuring only the part of the story that was easier to quantify.

Once Upon a Time, We Leaned Into Wonder

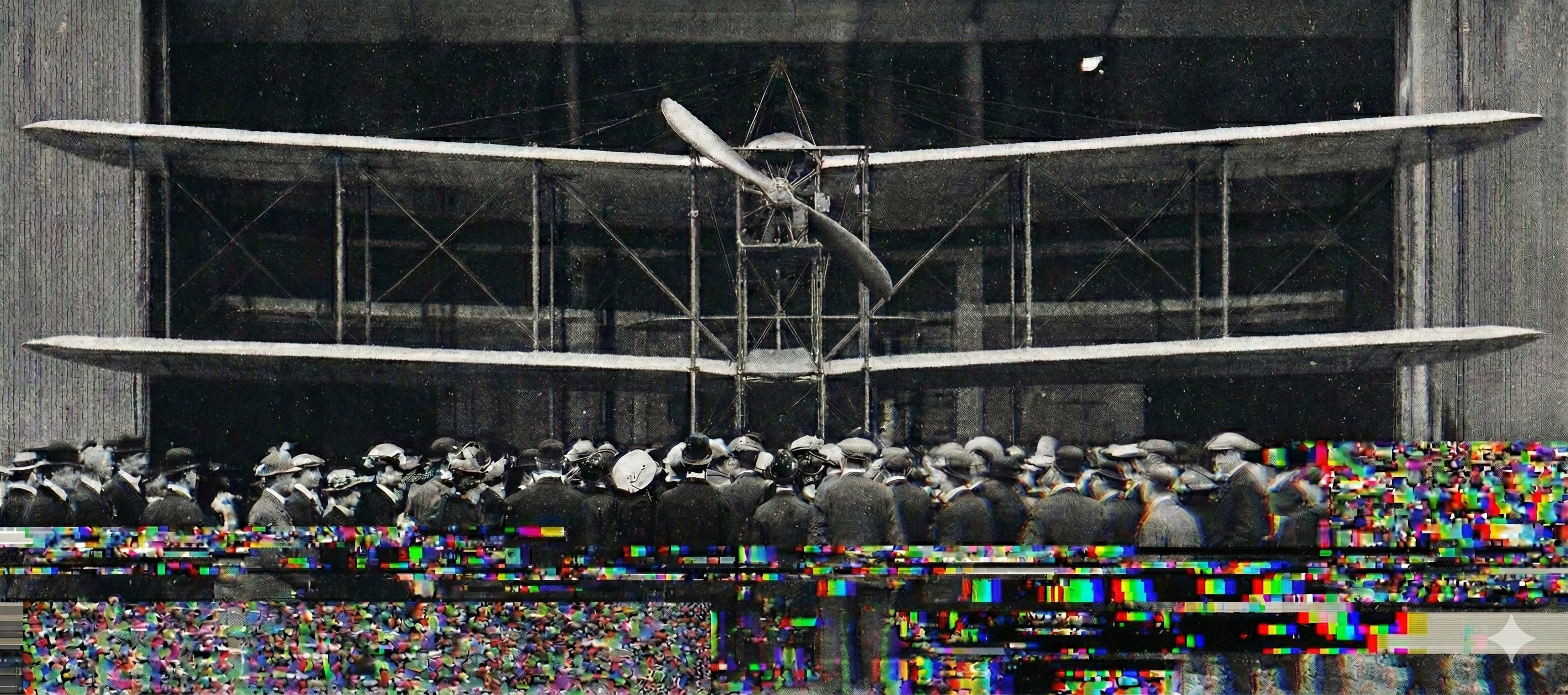

In July 1909, Harry Gordon Selfridge’s famous department store had been open for four months. He’d staked everything on a single idea: that shopping should be an experience worth having whether you bought anything or not. Wanderers were as welcome as buyers. You could come in, look at things and leave empty-handed, but you probably didn’t.

When Louis Blériot crossed the English Channel on July 25th, Selfridge moved immediately. Within days, Blériot’s monoplane — wire, ash wood, a 25-horsepower engine, still smelling of oil and canvas — was in the store window. 150,000 people came in four days to stand at the rope. Browsing through a store with a brain lit up with wonder? Cha-ching.

Simply being awed was the initial offer. The purchase was a byproduct. Selfridge understood emotion and resonance, he knew humans want to be inspired. Feeling something is a revenue driver, just not one that fits neatly in a dashboard.

Recently, I wanted to explore an author I’d been meaning to read. Ordinarily that would have meant surveying friends who knew my taste and going down a few search rabbit holes. Doing the kind of mapping that takes a bit of time and leaves you with a sense of the territory before you enter it. Instead, I asked an AI where to start. It gave me the most acclaimed work. It was excellent. But I came to it without the journey: without the early work that explained the obsessions, without the middle period where the style crystallized. Going back to the earlier work afterward felt like watching the highlights before the match. The AI answered the question I asked but removed the opportunity for me to arrive at a better question for how I like to explore like: what’s a good way in?

That’s what optimizing does. And it usually looks good…on paper.

Handing Over the Keys

My first inkling of what this would become started with comparison sites in the mid-2000s. Credit Karma, CreditCards.com, and the other aggregators turned years of card brand-building into rows of APR numbers and annual fees in a database. Brands that had invested in actual relationships found themselves losing ground to institutions that had learned to compete on the headline number, recouping it elsewhere in fees and terms the algorithm wasn’t designed to surface.

The real casualties were the consumers, of course. But the smaller lenders and credit unions didn’t fare well either. The credit unions lost the fight for billions in new customer spend not because their product was worse — quite the contrary in many respects — but because the aggregators were measuring the easy things, the wrong things, and therefore so were credit card shoppers.

The comparison table converted (huzzah), but it was reductive.

SaaS Marketing, Please Take Your Toys and Go Home

Enter DTC. The pitch turned idealistic: cut out the intermediary, build something people actually love, own the customer. We got more excited about “disruption,” “efficiency,” and “the model” than we did about the products. And the consumers? Just numbers going up or down on a spreadsheet.

Do you remember Fab.com? It launched in 2011 around an interesting idea: a daily design marketplace where the chief creative personally curated what went live. There were limited quantities, 24-48 hour windows, and objects you wouldn’t find anywhere else. The model was built around a question: what cool thing might I find today that I didn’t know I wanted? Within six months, a million people had signed up.1

Then Andreessen Horowitz arrived with $40 million. You take on that kind of money and growth targets are going to be the only thing you talk about. And, whatever model you were using is probably going to break as you try and achieve “scale.” In most cases, the pressure of that money means the very things that made a brand experience worth returning to will be eliminated. In Fab’s case this meant merchandising teams optimizing for volume and losing the cachet. The curated flash sale became a catalogue. The catalogue became a warehouse. The warehouse needed to move product. By 2013, Fab was trying to be the Amazon of design. At some point, they started selling steaks.

Traffic dropped 75% in under a year. Valued at $1 billion in 2013, Fab.com sold in 2015 for somewhere between $15 and $50 million. The founder wrote a memo to his staff: “I guided us to go too fast. I enabled us to lose our core focus.” The discovery was the product. Once it was gone, there was no reason to come back so people didn’t.

A decade after Fab’s fire sale, I launched a DTC menopause brand leaning beauty and lifestyle. Subscriptions were how we planned to justify what it actually costs to build a brand: the slower work, the development of narrative, audience, and advocacy. In practice, every tactic was optimized for the cart. Upsell, cross-sell, add-to-cart, you might also like. The whole architecture was oriented toward more sales without earning more attention.

And, the customer who receives something month after month without thinking isn’t loyal, they’re inert. Loyalty survives a better offer. Inertia doesn’t. Building the behavior without building the relationship is a very short-term strategy.

Marketing stopped being interesting (let alone fun) for years before I really understood why. None of this was sustainable. Extraction doesn’t compound. Relationships, however, do.

Stitch Fix followed the same old board-driven logic. Launched in 2011 on a genuine idea: human stylists who learned what you liked and sent you things you wouldn’t have found yourself. It IPO’d at $1.6 billion.2 Under pressure to grow, it built toward an “AI-first” model and in doing so, systematically dismantled the human styling layer and its point of difference. The stock is down more than 90% from its IPO price and it’s currently in a turnaround.

What Stitch Fix became was just another algorithm competing against Amazon’s recommendation engine and a proliferation of similar services. In a room where everything has to be quantified and is expected to become more efficient, what’s human gets optimized out.

Along Came Shopify

Shopify. The great enabler. In January 2026, Tobi Lütke — CEO and co-architect of the Universal Commerce Protocol — called the agentic era’s central promise serendipity. “I would have never searched for this product,” he said, “but somehow it found me.”3

What Lütke is describing is targeting. Serving things up. A passive customer experience.

Christian Busch, who’s studied serendipity for years, has a clear definition based on research and actual human behavior, not wishful thinking: luck happens to you, serendipity requires your participation, its an unexpected connection made by a person that went looking.4 Lütke didn’t go looking; the algorithm did, and presented him something accordingly. No discovery, just purchase. One builds attachment, anticipation, ownership. The other is just a brown box showing up on the doorstep.

The comparison site. The subscription. Now the agent. This is the Frictionless Trap: every step may feel like progress but this path strips away things we — brands, customers, investors — need.

BCG and Moloco found 33% of consumers now discover brands through AI agents.5 The Discovery Tax: the rapidly compounding cost of ceding how customers find you, was already accruing before agents arrived. This is when the bill comes due, and it’s going to be a doozy.

Go Put a Plane in Your Window

Gentle Monster, a South Korean eyewear brand, employs six people to design its glasses and sixty to design its stores.6 The stores are immersive art installations — kinetic sculptures, robots, themed environments that shift with each collection. You go for the experience and then you buy glasses. They’ve built something the algorithm cannot evaluate: a reason to walk in.

Glossier went back to what Emily Weiss had built it on — community, conversations, products developed from actually listening to what people wanted. Weiss had been pushed aside in favor of a growth model the brand couldn’t sustain. The recovery came from returning to the founder’s original instinct: the community is the product, the goods are the proof. By 2024, they were profitable.7

Both remembered that wonder (and wander) should be part of the offer.

The brands that will survive what’s coming are going to be the ones giving people a reason to form a relationship. That’s the investment the dashboard can’t measure and the agent can’t shortcut. It’s also, as it turns out, the only kind that compounds.

Selfridge didn’t remove friction. He put a plane in the window and wanted people to come see it.

Most brands stopped looking for the plane the moment the spreadsheet told them wonder didn’t have a conversion rate.

Footnotes

Fab.com founded 2011 by Jason Goldberg and Bradford Shellhammer. Raised $333.7M total. Reached 1 million members within six months. Peak valuation approximately $1B (2013). Sold to PCH International in 2015 for an estimated $15–50M. Goldberg’s internal memo to staff, October 2013.

Stitch Fix IPO, November 2017. Approximately $1.6 billion valuation. Founder Katrina Lake. Restructured toward an algorithmic model under investor pressure, reducing reliance on human styling. The company has faced sustained share price decline from its IPO valuation.

Tobi Lütke, quoted at the Shopify/Google Universal Commerce Protocol launch event, January 2026. UCP is a proposed open standard enabling AI agents to handle product discovery, cart management, and checkout across platforms.

Busch, C. (2020). The Serendipity Mindset: The Art and Science of Creating Good Luck. Riverhead Books.

BCG and Moloco, “AI is Collapsing the Marketing Funnel,” 2026.

Gentle Monster brand profile. Founded 2011, Seoul. 81 stores across 14 countries as of 2025.

Glossier profitability reported 2024. Emily Weiss stepped back from CEO role 2022; brand recovery credited to return to community-first positioning.

This is so good: “The discovery was the product. Once it was gone, there was no reason to come back so people didn’t.” That idea is that the core of this work. When the discovery is gone, why bother?